Beenos $3328.T

I wrote about #Beenos $3328.T several times and have become a fan for multiple reasons. Here is a more detailed article about my 2nd biggest position at the moment.

Q1 numbers will be released Feb 9

Key stats

Price 2355 Yen

MCap 29.8B Yen (=282M $)

EV 23.5B

EV/EBITDA 6.52 (LTM)

PE 15.6

PB 2.65

Business description

Beenos is a Japanese small cap in the e-commerce space. They have multiple platforms, which we will greatly simplify into these three categories:

1. Domestic Japanese e-commerce

Listed as “value-cycle” and “retail and licensing”. These businesses suffered from covid and the stagnant market of Japan.

2. Exports from Japan

Japanese goods are sold globally, see “cross-border” below.

3. Apart from these operating entities, Beenos also has a very successful investment branch (“incubation”).

Thesis

- High growth, high margin subsidiary “Buyee” is hidden in statements

- Investments could be worth more than the MCap

- Cash rich + low valuation provides downside protection and room for valuation increase

- positive forecast +30% op. income

Unimpressive from the outside

The financials show a boring company with stable revenues, very erratic income and a seemingly bad quarter with revenue and income down.

Yet, the stock price jumped almost 50%, let’s see why:

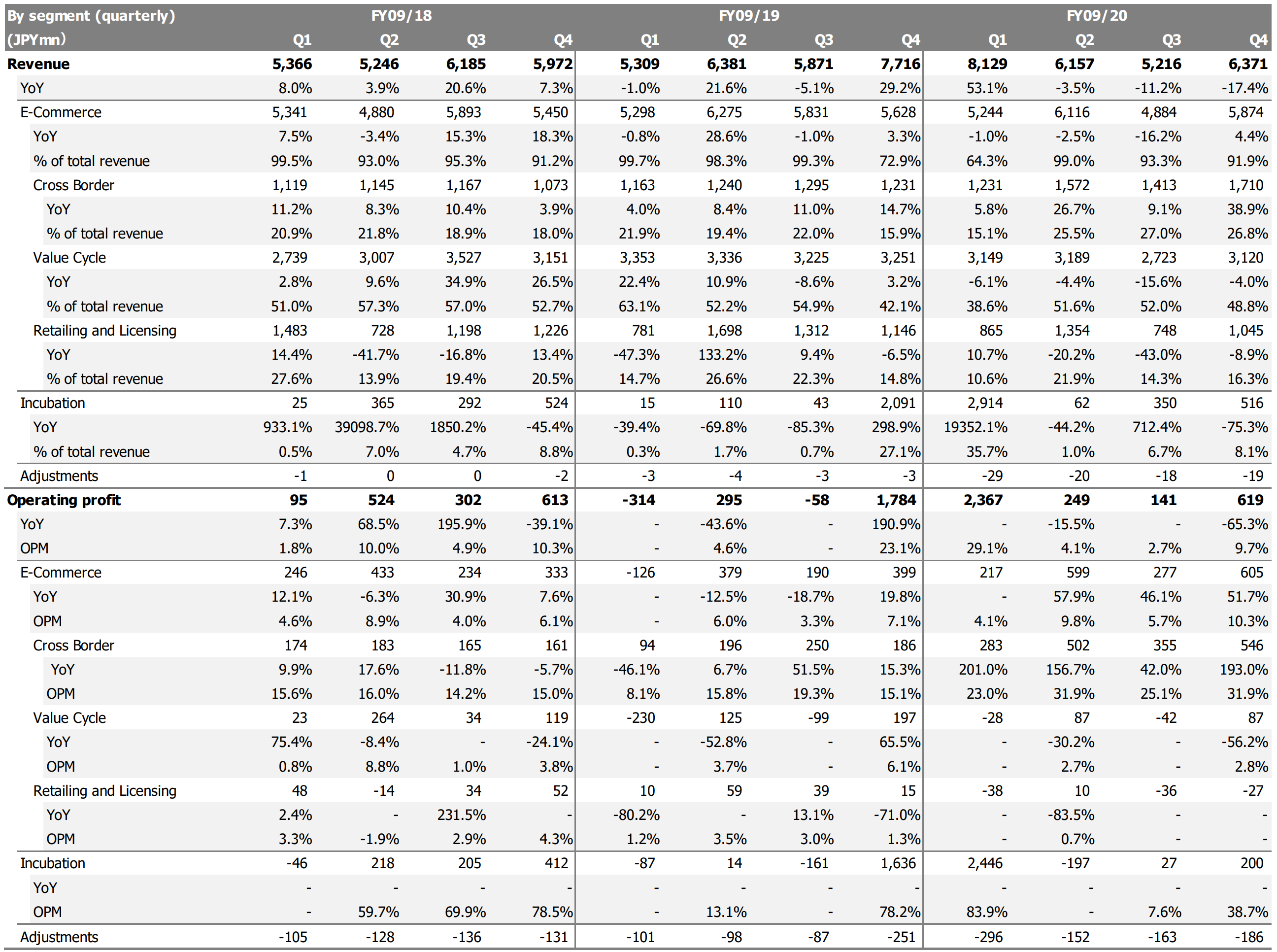

Recent Q4 numbers in the last column:

Let’s forget domestic Japan (="retail" + "value cycle"), which has fallen from 80% of revenues to 65.1%. Operating profit of these two segments is 87M-27M=60M Yen

—> value right now = 0

”Buyee” and the cross-border business:

26.8% of total revenues = 1710M, growing 38.9% YoY

op. profit=546M, +193% YoY

huge margin 32%

Buyee is a c2c marketplace for buying Japanese merchandise (like anime, games) from all over the world. Buyee provides the shop, communication, payment, shipping, everything and gets a flat fee.

A partnership with SEA's ($SE) Shopee boosted tremendously. They recently added Russia and China to their list of customers.

Changing their fee model from % wise to a flat fee further increased their margins.

First recap:

Beenos’ stagnating legacy business is a major part of financials - clouding the high-growth high-margin export business. Buyee and the whole "cross border" part alone is worth the current EV:

EV 23.5B Yen

Rev 5.93B Yen

Op. profit 1.68B

growth accelerating, positive outlook (+30% profits)

Small caveat: Management said, that Q4 had positive one-offs

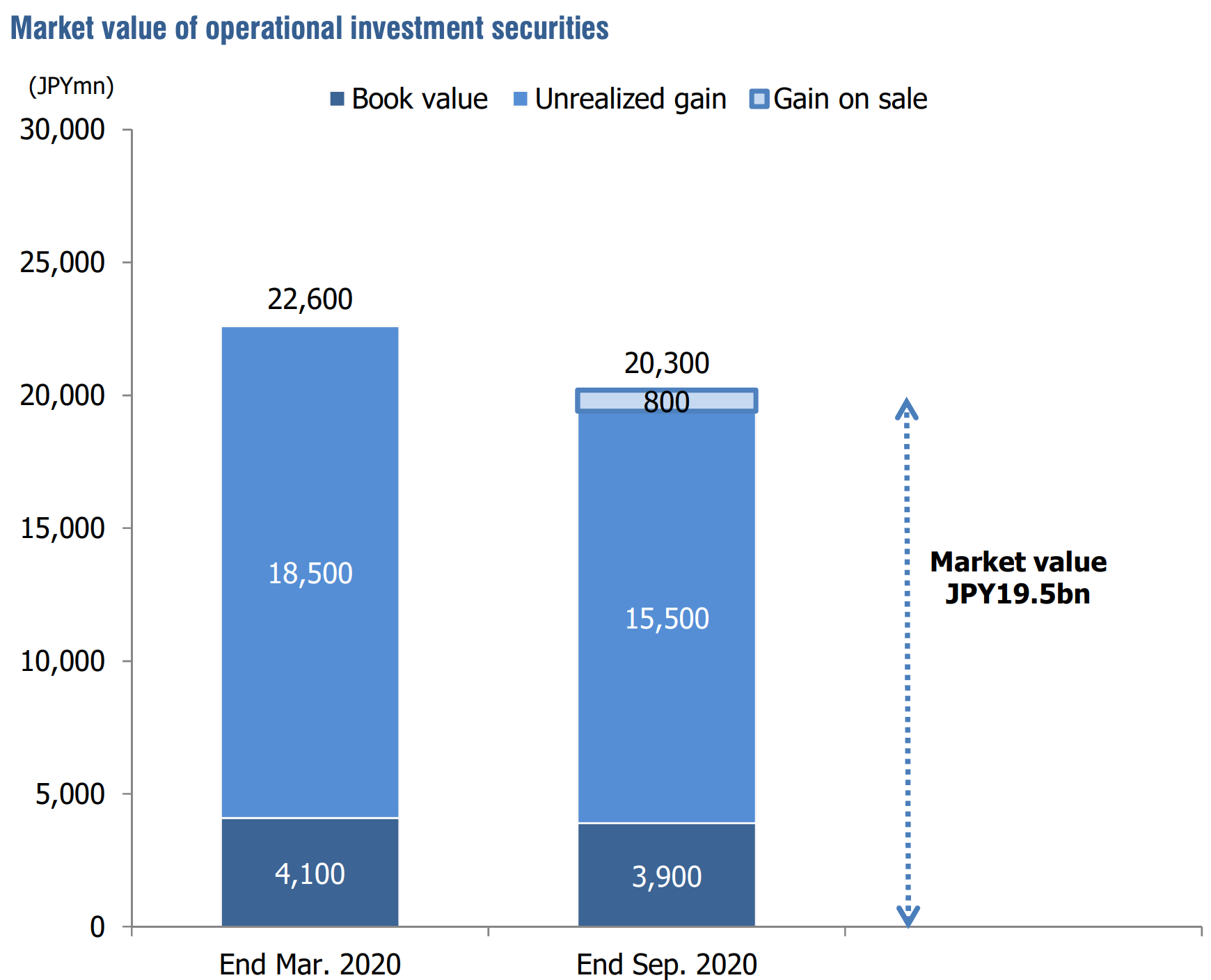

Investments at book value?

The story does not end here: Beenos has around 10B cash - debt = 6.3B Yen net cash.

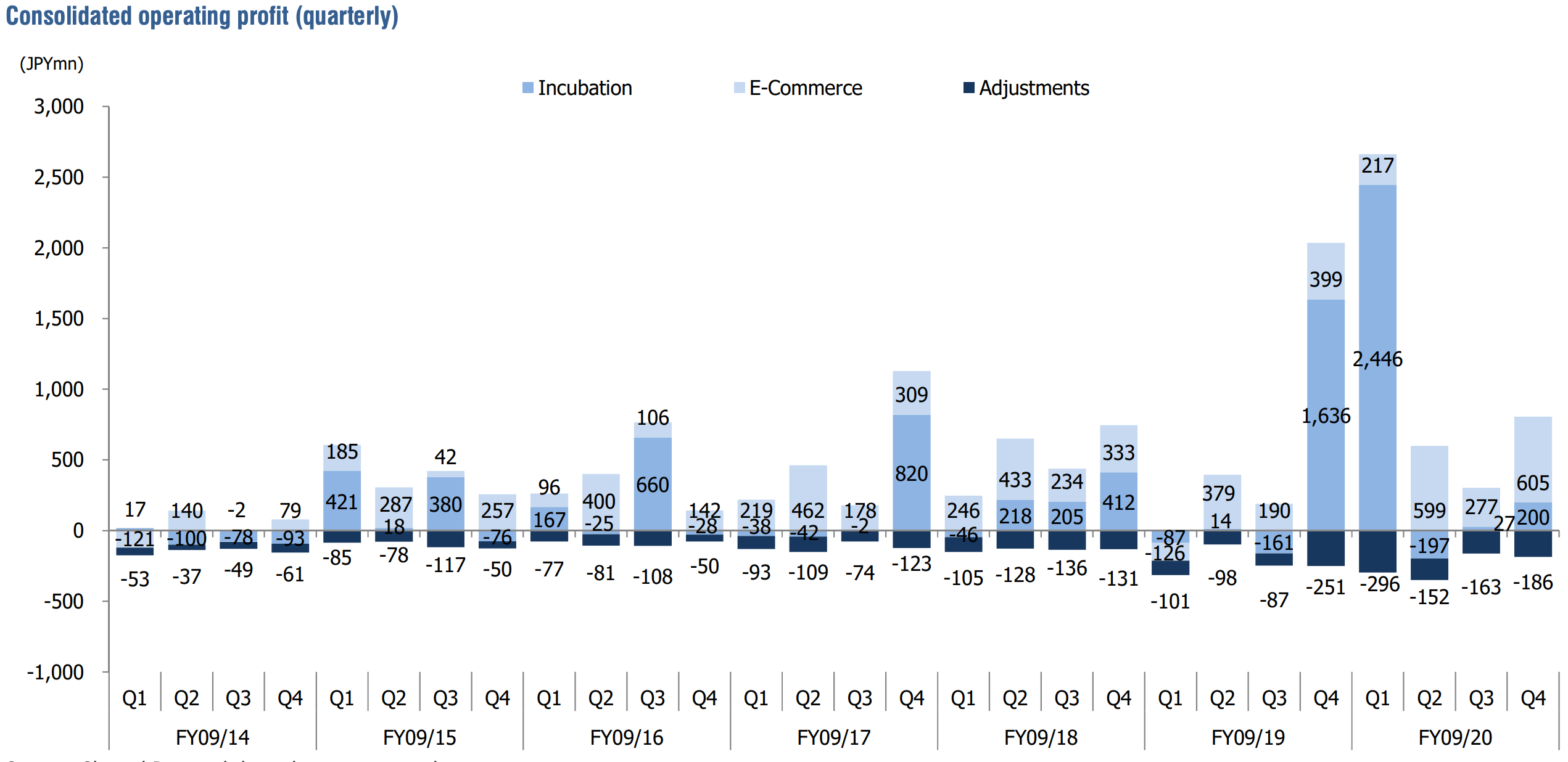

Where does the money come from? Selling investments they mainly entered 5-8 years ago when they revamped the company. Their focus is the e-commerce and payment sector of Asia.

This chart shows the investment gains, named "incubation", providing the bulk of long-term gains. Big sales occurred in Q4/19 and Q1/20 and management is actively focusing selling their stakes. Ecom and payments in Asia has been and still is a very hot sector.

But are there still arrows in the quiver?

Yes, Beenos states, that their investments carry at book value of 3.9B, yet are valued at market at around 20B Yen. Remember: EV of Beenos is around 23B Yen.

Their main star is their stake in Tokopedia (0.5 - 5%, rumors say 2%), the “Indonesian Amazon”. It is in talks to go public via SPAC backed by Peter Thiel and Richard Li and is valued at 8-10B Dollars. Other stakeholder are Softbank, Alibaba and Google.

Forecast and Summary

Beenos has given a positive forecast, but explicitly excluding “incubation”, as they are in the process of selling more investments.

Their legacy business should provide a black zero, the cross-border (renamed to “global commerce”) is aiming at +27.5% operating profit.

In summary we have several factors that should greatly benefit an investment in Beenos:

- Buyee and the “global commerce” is hidden in the financial statements

- Buyee is a high growth, high margin business not reflected in the share price

- Their investments have been highly profitable and spot on in the past and the best is yet to come: Tokopedia

- They still have lots of other investments that are listed at book value far below their current valuation

- Very low downside because of net-cash and the fact it is a growing and profitable business,

- High upside because of several catalysts

Sources

blog post by @WillThrower3

https://dumilecapital.com/2020/08/11/3328-beenos-strong-growth-deep-value/

SharedResearch

https://sharedresearch.jp/en/3328

Beenos IR

https://beenos.com/en/investors/ir-news/

Forgot about this stock for a few months and my jaw dropped at the stock price. Seems like the Goto investment should more than cover the enterprise value of the stock. They also initiated another buyback. Indiscriminate selling?